Recent News

-

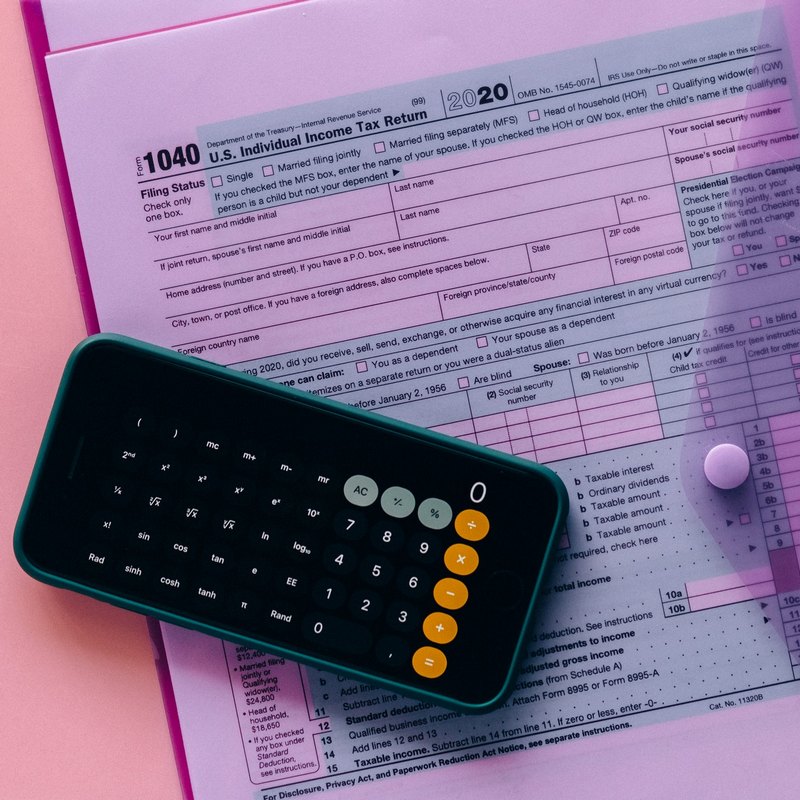

Tax Guide: All You Need to Know About Taxes

2022-10-24

-

Everything You Need to Know About Income Tax in Canada

2022-07-17

-

Other Taxes

2021-02-17

2022-10-24

2022-07-17

2021-02-17

Tax & Finance Blog

![]() Non AAMS casinos are not regulated by the Italian Gaming Commission. However, this does not mean that it is not safe to play at these sites, as most non AAMS casino sites are licensed by the governments of other countries, the most popular being Curacao and Malta.

Non AAMS casinos are not regulated by the Italian Gaming Commission. However, this does not mean that it is not safe to play at these sites, as most non AAMS casino sites are licensed by the governments of other countries, the most popular being Curacao and Malta.

More than 3,000 tutors are available online to assist you with the most difficult problems. Our tutors can accounting homework help you with all levels of accounting, even college accounting homework.

Welcome the new slots 2021! Hit the jackpot on new slot machines and get big slots payouts every day when you play online slots machines for free – Casinos online Brasil

Tax season is coming. Make sure to use Genesa’a tax consultants in Vancouver, BC to get the best accounting service.

Online casino Goxbet or Goxbet 4 (brand name now) has been working in Ukraine since 2015. Follow the link, find out how to log in Go x bet, register, get bonuses and which slots are better to play and which providers are top.

Are you looking for an online casino platform that’s filled with lots of casino gaming options? 1win casino is an online casino platform that has different online casino games, live casino games, and even jackpot games.

Get ready to take your gambling adventure to the next level! Embrace the excitement and freedom at a casino operating without a Swedish license. Discover a world of unparalleled possibilities at utansvensklicens.casino – where luck and skill intertwine, paving the way to unparalleled rewards and electrifying wins!

Finance research papers, calculations, equations, you name it. You can choose the best research paper writer who will tackle any of those tasks.